Some of you reading this short note are either living in Devon or have previously travelled down to Devon for a lovely trip amongst the rolling fields, moors and beautiful beaches of this somewhat remote county. For those who live in Plymouth and the surrounds, or are familiar with this famous naval seaport, you will know that it was once home to Sir Francis Drake (that famous Elizabethan pirate who so vexed our Spanish friends by stealing their gold) and that Plymouth was also the site of the departure of the Mayflower with the pilgrims on board heading to America 400 years ago this year. Less of you will know that it was the place of an amazing insight into the powerful nature of crowds, which provides us with a wonderful word picture of how markets operate.

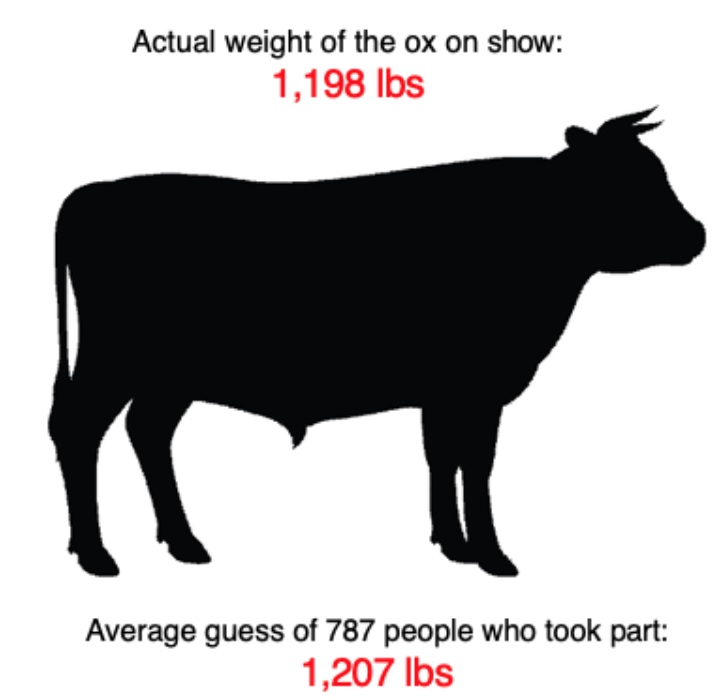

In 1906 a Victorian gentleman named Sir Francis Galton attended a livestock fair aptly named The West of England Fat Stock and Poultry Exhibition in Plymouth. One of the many attractions at the fair was a guess the weight of the ‘dressed’ ox on display (similar to the game of guessing how many cookies are in the glass jar). The competition attracted 800 people all paying 6d (half a shilling) to write down their guess, name and address on the back of the ticket. The nearest guess to the actual weight would win a prize. The fair, as you can imagine, attracted many sorts, from the general public, old and young, to farmers and butchers. Being a statistician, amongst many other things, Galton bought the used tickets off the stall holder. Of the 800, 787 were usable. Back home he analysed the guesses and published his finding in Nature, March 7, 1917 in an article titled ‘Vox Populi’. His remarkable finding is illustrated in Figure 1.

Figure 1: Guessing the weight of the ox – the ‘crowd’ got it more-or-less spot on

Source: Albion Strategic Consulting

The range of guesses was wide (-133 lbs. below the average to +86 lbs. above it), the participants were varied, and the numbers involved were quite large. The ‘crowd’ in aggregate showed ‘wisdom’ compared to its individual participants.

This story provides a great insight into how modern financial markets work. The markets are made up of many players, from individual DIY investors, day traders, stockbrokers, hedge funds, fund managers, sovereign wealth funds, endowments and other institutional investors. Each investor holds their own view on the future prospects for a specific security, such as the price of BP or Apple shares. Some will like a stock and others not. They cannot both be right. The market, given all the information available to it, settles on an equilibrium price for every stock. This price will move, sometimes dramatically, as we have seen recently as the ‘market’ reaches a new equilibrium price, given the new information that it has collectively processed.

At times like these, some investors are prone to running ‘what if’ scenarios in their heads such as: ‘if companies are in trouble because their revenues have been cut off, then they will renege on their property lease terms and the landlords will suffer. It seems likely that things will get worse over the coming weeks. If property landlords are in trouble that might lead to problems in the banking sector’.

It all sounds plausible. They may then be tempted to sell out of property or banks or even equities altogether. The crucial mistake is that they forget that they are not the only person to have thought this through and these very sentiments and views are already reflected in the current price of listed commercial property companies, bank stocks and the markets in general.

Markets will move again, down or up, based on the release of new information, which in itself is random. Second guessing random events is futile. You may make a guess and be lucky but that is speculating not investing. Accepting the ‘wisdom’ of the market helps us to challenge ourselves as to whether we really have superior insight relative to everyone else. It seems unlikely. As Charles Ellis, the wise sage of investing from the US, states:

‘In investing, activity is almost always in surplus’.

Activity based on guessing, particularly when it relates to shorter-term issues that sit well within your true investment horizon, is best avoided.

Next time you pass Plymouth on the A38, reflect on one of its great historical events, The West of England Fat Stock and Poultry Exhibition of 1906.

Note: if you are interested in this subject and have time to fill in the coming weeks, perhaps take a look at The Wisdom of Crowds by James Surowiecki published by Greener Books.

1. You can view the original article here: http://galton.org/essays/1900-1911/galton-1907-vox-populi.pdf